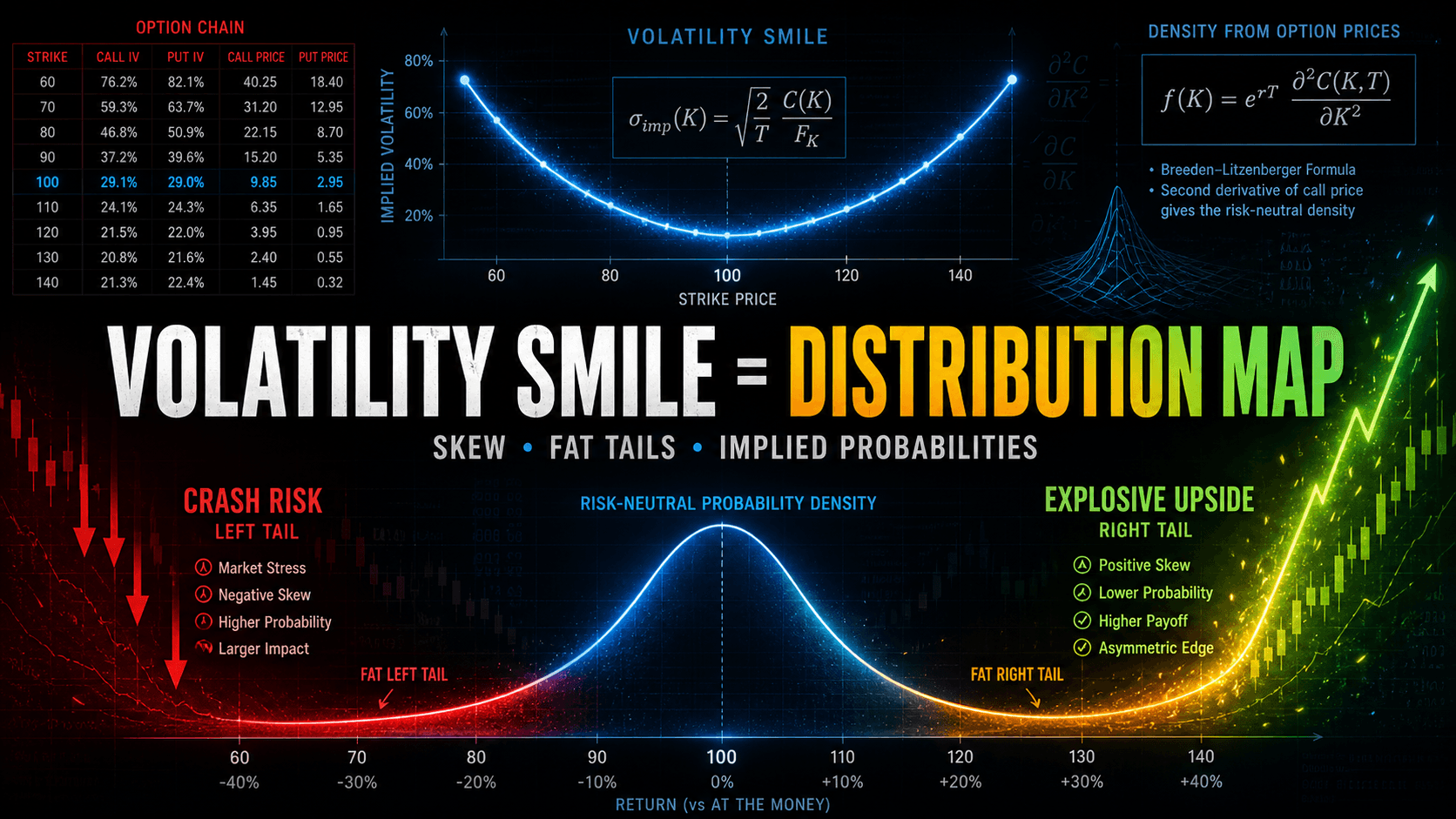

Volatility Smile as a Distribution Map

Apr 22, 2026 - Tribhuven Bisen

Volatility skew and the smile reflect the market pricing in asymmetric, fat-tailed risks—capturing crash fears and rare upside events rather than a simple lognormal distribution.

Intuition Behind Skew and Fat Tails

The volatility surface is a forward-looking representation of the market’s risk-neutral probability distribution of the underlying asset.

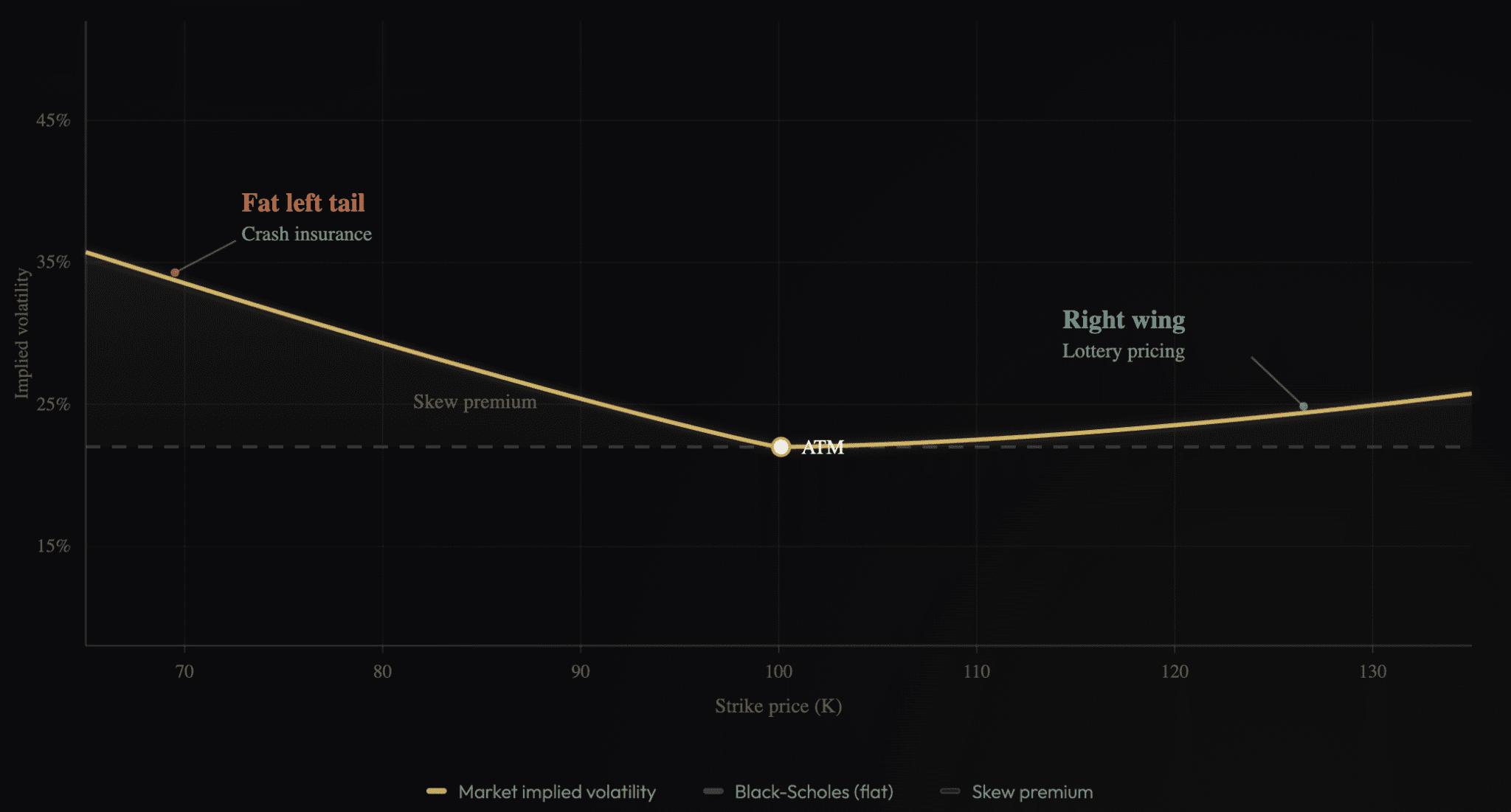

While the Black–Scholes model assumes a lognormal distribution of returns and a flat volatility surface, empirical observations consistently show pronounced skew and kurtosis, often described as the “volatility smile.”

1. Option Prices Encode Distributions

Under risk-neutral pricing, option values can be expressed as discounted expectations of payoffs:

Risk-neutral pricing representation

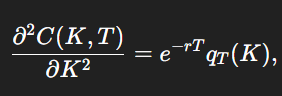

where C(K,T) is the call price at strike K and maturity T. Differentiating twice with respect to strike yields the risk-neutral density:

Extracting risk-neutral density

where qT(K) is the implied probability density of ST. Thus, the curvature of the option price surface reveals the underlying distribution.

2. Symmetric vs. Skewed Distributions

Two stylized cases highlight the connection:

Stock A: 50% probability of doubling to 200, 50% probability of going to 0. This symmetric distribution around 100 generates moderate option prices and relatively flat skew.

Stock B (biotech case): 90% probability of going to 0, 10% probability of surging to 1000. Despite the same expected value (100), option prices differ dramatically. Deep out-of-the-money calls are highly valued, producing a strongly right-skewed implied distribution.

Both assets have identical spot prices, yet their option surfaces encode distinct higher moments (skewness and kurtosis).

3. Smile as a Map of Tails

Empirically, equity index options display downside skew:

- Out-of-the-money puts command high implied volatility, reflecting the market’s pricing of crash risk (fat left tail).

- In certain sectors (biotech, technology), out-of-the-money calls are also expensive, encoding rare but explosive upside (fat right tail).

The volatility smile is therefore not a model failure, but an adjustment: markets systematically assign greater probability mass to tail outcomes than a lognormal distribution would imply.

Practical Implications for Trading

-

Skew encodes crash risk: OTM puts are expensive because markets consistently overweight downside tails.

Selling puts = short crash insurance. Expect high carry but tail blowups. -

Calls as lottery tickets: In skewed distributions (e.g., biotech, tech growth, crypto), far OTM calls trade rich.

Buying calls here is not irrational — it’s priced exposure to rare but convex payoffs. -

Why Vega ≠ full story: Traders often focus on Vega (sensitivity to vol), but the shape of the smile matters more.

Example: A 25-delta put can be “overpriced” vs ATM vol but still reflect structural demand (hedgers, insurers). -

Smile ≠ arbitrage: A flat Black–Scholes smile is not “truth.” Skew reflects the reality of fat tails.

Attempting to fade skew mechanically is dangerous — you’re betting against structural flows and crash insurance buyers.

4. Trading Tips from Practice

-

Use smile analysis to choose structures: If the skew is steep, put spreads often offer better risk-adjusted carry than naked short puts. Calendar spreads can isolate whether skew is term-structure driven or event-driven.

-

Look for misalignments across strikes: Compare implied densities via butterflies. Outliers often point to overpriced insurance or underpriced tail optionality.

-

Respect path dependence: Gamma exposure around skewed strikes is dangerous. Moves into the skew (e.g., spot falling into heavy put OI) can force market makers to hedge aggressively, amplifying moves.

-

Context matters: In indices, skew is mostly left-tail crash risk. In single names, skew can be both downside protection and upside lottery pricing.